1. Introduction

Healthcare in developed economies is becoming increasingly unaffordable. This is being driven by a combination of factors including:

-

an ageing population with their greater demand for healthcare.

-

technology, especially the growth in the range and costs of treatment and diagnostic tools.

-

the spiralling cost of trained staff, buildings and other infrastructure.

The latter two improve individual outcomes but at increasing cost to the taxpayer. To counter this trend, we argue that health systems need to concentrate more resources on prevention: that is, preventing illness in the first place, to keep people as healthy and productive as possible for longer. This is also the message of the new Labour Government and is a key part of its health strategy.

However, the term “prevention” is misleading because it has more to do with disease avoidance or risk reduction than its complete elimination. Interventions designed to reduce risk of ill health or death therefore come in many forms, and measuring their effectiveness is challenging. There are few silver bullets, and consequences may be both intended and unintended.

History holds several examples of interventions that have made substantial improvements to population health, such as housing, clean water supplies and the introduction of universal education. These led to significant improvements in life expectancy and reductions in deaths from diseases of poverty such as tuberculosis. Most can be linked to the passing of legislation at the time but were not the primary reason they were enacted.

An intervention can be thought of as the alteration of exposure to a given risk factor that does not necessarily prevent an outcome’s occurrence, but which may reduce or postpone it or protect lives and property. The population affected by any given risk can range in size from the entire population and/or be specific to individuals with certain characteristics. Most interventions have a defined purpose or measure of success.

For example, reduced tooth decay by fluoridated water is an example of a population-wide intervention. It involves adding prescribed amounts of chemicals to water to keep it safe to drink and is considered to have been highly effective since its introduction in the 1960s in the UK. Water chlorination to prevent waterborne disease is another example with earlier origins in the 19th century.

At the individual level, prevention involves personal choice, such as whether to smoke, despite evidence that it is harmful to health and life expectancy. For government, the interventions range from doing nothing or banning its use in public places to increasing its price or banning its sale altogether.

Universal interventions through taxation can be deeply unpopular because they adversely affect business and people’s enjoyment: for example, the drinking of alcohol. However, this must be weighed against the harm alcohol causes from liver disease, increased anti-social behaviour, domestic or other violence, increased health spending and premature death.

Interventions aimed at reducing exposure are similarly varied but nearly always need to strike a balance. The forced closure of pubs, for example, would be seen as extreme, but increasing duty on alcohol less so. More subtle interventions such as reducing the alcohol content of beverages may be a better way forward. The growth in popularity of non-alcoholic beers and wines is a relevant example.

The use of medication is a type of intervention that is typically deployed once a disease is established, either to cure it, prevent or delay its recurrence or worsening or for controlling pain. From a prevention point of view, medication is becoming increasingly common; one important example is the use of statins for lowering cholesterol.

Another recent and topical example involving medication is drugs to promote weight loss. Obesity is a major threat to health, affecting both employment prospects and shortening life expectancy. Drugs such as Wegovy or Ozempic are effective at inducing weight loss and constitute a growing market – the irony is that in this case drugs are being used for controlling a condition that is generally manageable through diet and physical exercise.Footnote 1

Examples of medication also apply in the case of infectious diseases, such as the use of chemoprophylaxis drugs given to travellers before entering areas with malaria, which can be highly effective when combined with insecticide-treated nets. The development of a malaria vaccine now being trialled in affected areas is ultimately the long-term solution to this major problem.

The successful introduction of other vaccines around the world is directly responsible for the reduction in deaths from a range of infectious disease and increasing life expectancy globally. Vaccines can cut the risk of a particular disease for life, as in the case of polio or smallpox, but lifetime protection may require regular vaccination for diseases such as influenza or COVID and may not be as effective.

The temptation is to think of exposure to one risk factor at a time, but context is important depending on personal circumstances, environmental and other factors. For example, there is no need to vaccinate against a disease such as Ebola in non-exposed regions or build flood protection in deserts, to give two examples. It depends on the scale of the threat.

2. Preventive Benefits of Non-Medical Interventions

In general, a holistic approach is preferable, considering not only the primary risk factors but also ambient or accompanying risk factors. These may be biological as well as social, economic and psychological in origin. A rush to medication, for example, may be less cost-effective than a policy of risk factor management.

Risk factors are interconnected in ways not fully understood. Thus, root causes of income inequalities can work in both directions – because of ill health or due to the prevalence of poverty leading to ill health. These may be hard to disentangle, although there may be patterns in the data giving a strong indication, for example, where the population affected is well-defined, such as low-income families.

Examples of gaps include the health benefits of good quality homes for ageing persons, employment or communal living. Knowing whether you will live longer and healthier in a retirement community or engaging in physical exercise or sport seems important if the evidence is relatable and authoritative. In these cases, interventions are not healthcare related.

In the wider public sphere, there are many examples of interventions that support the work and activities of local authorities, social care providers and the third sector. These include help with heating homes, tending to gardens or small house repairs or health advice where outcomes are measured in fewer general practice (GP) visits, Accident and Emergency (A&E) attendance or hospital admissions.

The design of interventions is important. For example, timelier assessments and partnering with the third sector and private providers helped one local authority to reduce the number of bed-days by between 14 and 28 per person among older persons and by up to five A&E attendances (Mayhew, Reference Mayhew2009). Previously, these arrangements were bogged down by a lack of information-sharing and delayed social care assessments.

In another study, Mayhew and Harper (Reference Mayhew and Harper2019) found that for women aged 16 to 64, average secondary care costs increase by £232 if they live in a benefits household compared with a non-benefits household, by £108 if they are current or ex-smokers and by £90 if they live in social housing. The study also showed costs were significantly higher for people if they lived alone or in a one-parent household.

The general point is that some risk factors are more modifiable than others. Public health experts discuss wider determinants of health as well as direct or proximal causes, of which the above are just a few examples. Their identification can often lead to improved efficiency at lower cost, especially if the alternatives are costly medical interventions lasting a lifetime.

It is fair to say that actuaries have not engaged in prevention to any great extent for reasons set out below, although the link between prevention and risk – a key actuarial tool – is very strong. Our purpose is to redress that balance using ideas from everyday life, from a value-for-money or productivity perspective and thus enhance actuarial visibility and the contribution it makes to society.

2.1. The Measurement of Cost Effectiveness

In this paper, we are interested in interventions that are primarily lifestyle related. These include social experiments relying on combinations of inducements, either financial or persuasive. The analytical challenge is to design experiments for which costs and benefits can be accurately evaluated and are statistically sound.

There is a plethora of methods that usually involve comparing a group that has been exposed to one or more risk factors to another that has not (e.g. see Glover & Henderson, Reference Glover and Henderson2010). Randomised control trials, for example, are impractical at a population level for reasons of cost, ethical and other factors, but are the gold standard for evaluating new drugs.

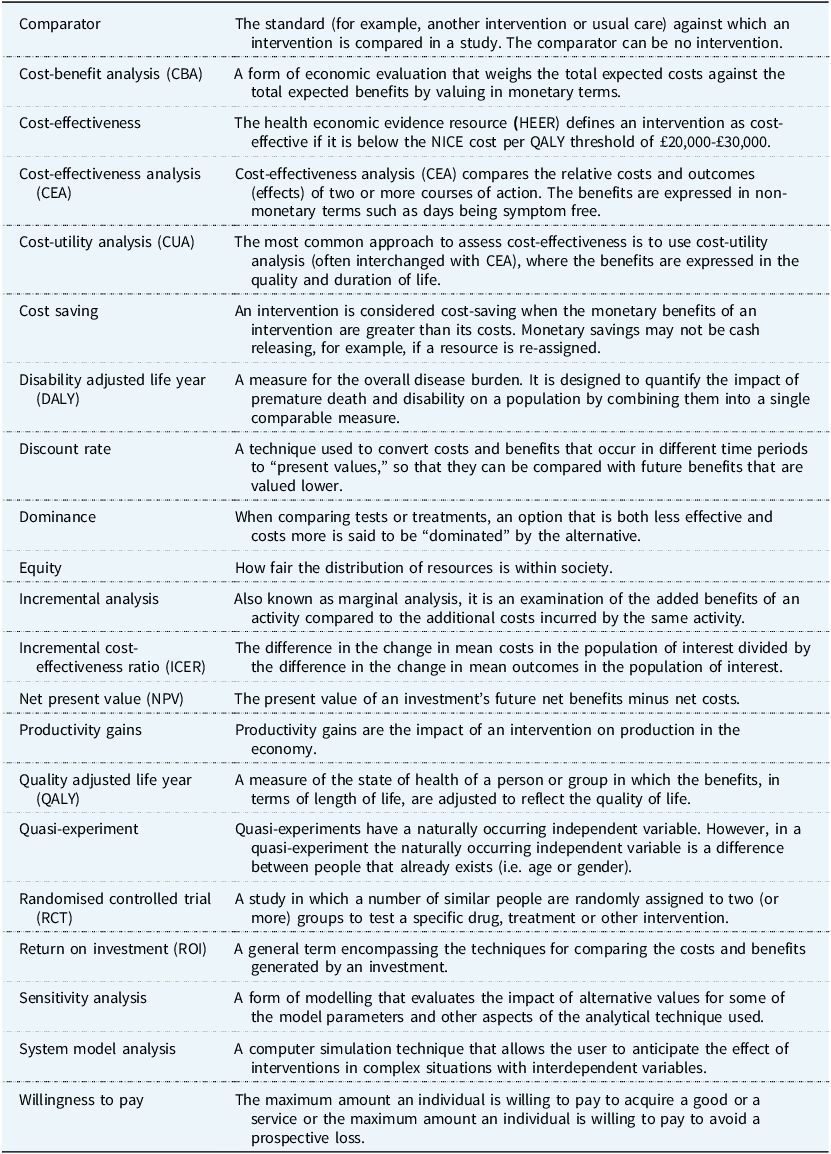

A glossary of terms used in cost-benefit studies applied to prevention is available from Public Health England.Footnote 2 It has worked examples covering topics like sexual health services, National Health Service (NHS) health checks, weight loss programmes and physical activity, alcohol misuse, drug misuse, smoking cessation and others. Table 1 gives the details of these.

Table 1. Terms typically used in prevention studies (source: Public Health England)

Key issues are time-varying costs and benefits that may vary with exposure. An intervention that is expected to pay for itself within five or ten years, say, may fail if a subject dies sooner. Evaluations are usually based on the cost per Quality Adjusted Life Years (QALYs), which are a way to combine quality of life and life expectancy into a single index.

To calculate QALYs, each health state is given a utility value that reflects the quality of life associated with that state expressed as the number of healthy years resulting from a new drug or other intervention. The National Institute for Clinical Excellence uses QALYs to justify whether a new drug should be paid for by the NHS; the cost per QALY gained needs to be less than £20,000 to £30,000 to qualifyFootnote 3 .

Cost-benefit applications typically include both the direct and indirect impacts on the public purse and society. These divide into those that lead to improvements, such as more patients treated versus the cost of an intervention. They include the direct health costs incurred by the NHS and related services such as social care, whilst indirect effects include many elements from changes in employment to welfare benefits.

One example is a tool for measuring the financial benefits resulting from a return to work after a period of inactivity – for example, for people with common mental health disorders. The tool allows local decision-makers to understand the health and financial impacts, for their local population, of getting people back to work (Public Health England, 2017).

Applications of cost-benefit analysis within the insurance industry are fewer. They focus on the insured population and prioritise individual risk using policyholder data (albeit informed by experience in the general population), mortality and epidemiological data and previous claims. The emphasis, however, will be different depending on the insurance product.

For example, insurers base premiums on their evaluation of the probability of an event occurring such as a critical illness, absence from work due to sickness or loss of job in the case of income protection insurance or death itself. Premiums may be one-off or vary from year to year depending on claim history and costs, as is the case with health insurance.

The question is whether there is a public good element involved. In the annuity business a person dying sooner profits the insurer but causes a loss for a life insurance provider. In health insurance, treatment paths are circumscribed and budgeted. Prevention plays a negligible role; there is no obvious reason why an insurer should be concerned with anything other than risk.

Premium ratings are sensitive to age, where you live, your job and so on. In some instances, insurance companies may offer rewards such as gym membership or reduced premiums for healthy behaviours, for sticking to approved lifestyle routines as set out in the policy contract or via other mechanisms such as health checks.

However, any link to prevention is tenuous at best and there is no public good as such. A different model is one where doctors are only paid if you are healthy and compensate you if you are not. This is not far fetched; capitation fees are common in general practice and theoretically reward practices with healthy lists, so there is a preventive element – albeit an indirect one.

Proof of effectiveness for insurers is ultimately judged according to sales and profits. The direct contribution by the industry to prevention is therefore currently small. However, the message of this paper is that there are reputational advantages in increasing public engagement with prevention using its actuarial expertise and working more closely with the public sector.

The availability and quality of data will vary according to the topic of interest and the methodology. This can include administrative sources, official statistics, surveys, commissioned data collections or uses of social media data, which is a relatively new source of information. If person-identifiable data is accessed, it needs to be de-identified before use.

The cost side of the analysis is at least as fraught because of the need to include the indirect costs or savings from courses of action for which data are very limited. The Green Book (H.M. Treasury, 2022) is HM Treasury’s guidance on how to appraise policies, programmes and projects, both before, during and after implementation and is essential reading.

3. The Cost of Smoking-Attributable Risks

In this paper, we use smoking as our prevention case study. Whilst smoking is in decline, it still kills approximately 78,000 people a year and reduces life expectancy by around 10 years, but also shortens health span (Mayhew et al., Reference Mayhew, Chan and Cairns2023). As well as cancer, it is associated with other harmful behaviours such as excessive alcohol use and mental illness and is a key cause of health inequalities.

The history of smoking is an object lesson in amassing the evidence needed to fight vested interests and political indifference and spurious arguments based on restrictions to freedom, which ignore consequences such as economic loss, earlier death and increased healthcare costs. Cost-benefit analysis offers a template for how to value prevention by attributing costs and benefits among stakeholders: in this case, the individual, state or economy.

For example, Mayhew et al. (Reference Mayhew, Chan and Cairns2023) show how a complete ban on smoking would lead to a 2.5-year improvement in healthy life expectancy after considering already lapsed smokers. It found that economically active smokers tend to be less productive, more so in their later years, in addition to various health conditions. Socio-economic factors such as low educational status and income deprivation are further correlates.

The same research finds that the loss to UK GDP is of the order of £20bn a year from the employment effects of smoking-related inactivity measured in lost earnings. Other attributable costs, like adult social care and welfare payments, tend to be hidden from view or ignored. The next sections explore these effects in further detail.

3.1. Societal Impacts of Tobacco Consumption

In what follows we drill down into a detailed case study on smoking. As well as drawing on our own findings, we draw on the wider literature and on especially commissioned research by action on smoking and health (ASH)Footnote 4 , which is a public health charity receiving funding from the British Heart Foundation, Cancer Research UK and the Department of Health.

Despite the falling prevalence of smoking and reductions in deaths from smoking-related diseases, hospital admissions due to smoking-related causes have been increasing. This is partly a response to an aging population and the lingering health risks to lapsed smokers, which means they spend more years in ill health prior to death at younger ages.

Health costs increase with age, but data do not generally distinguish between smokers and non-smokers. Figures from the Office for Budget ResponsibilityFootnote 5 show that the average annual cost of healthcare increases from a low of around £1000 at age 20, rising steeply to £9000 at age 90 (4.5 times higher than at age 60).

These differences are especially important given that the UK population aged 65+ is projected to rise from 12 million to 17 million by 2040. It means that the difference between a smoker who dies sooner and a non-smoker who dies later but still incurs healthcare costs could become a significant consideration, especially if long-term care costs are involved.

Differences in healthcare costs by age are reported in a Danish study (Rasmussen et al, Reference Rasmussen, Søgaard and Kjellberg2021) which shows average healthcare costs rising with age, but more steeply among current compared with never smokers, as shown in Figure 1. The same study finds that lifetime healthcare costs (including discounting) of smoking for an 18-year-old man were €10k less for a non-smoker and €6k less for a woman.

Figure 1. Average annual healthare costs by age for Danish males (Rasmussen et al, Reference Rasmussen, Søgaard and Kjellberg2021).

The Danish healthcare system largely mirrors the NHS in that it is free at the point of use and so makes for a good comparator. However, these differences are smaller than one might have expected. Reasons for this could be:

-

The healthcare and treatment costs associated with poor health due to smoking-related diseases might be lower than those for the diseases affecting non-smokers later in their lives (e.g. dementia).

-

Discounting has the effect of giving more weight to smokers who die sooner and for whom healthcare costs are incurred earlier.

-

For a majority of people, their lifetime health costs occur in the last year or two of their life. For non-smokers, this will be later in absolute terms, but the end-of-life costs remain.

The Danish study also evaluated the lifetime net excess public expenditure costs, taking social care, income and tobacco taxes into account. Results showed that a non-smoking man had lifetime earnings €90k more than a current smoker and net public expenditures that are €20k lower. For women, the equivalent figure for net public expenditure was that it was lower by around €10k, but it noted that this was attributable to lower lifetime earnings.

The researchers used survey data on smoking status, alcohol consumption, body mass index (BMI) and physical inactivity, which they then linked to Danish registries on their health and home care costs, educational status, earned incomes, public expenditures and tax payments. This is a step up from what is possible in the UK, where registries do not exist, but there are similar surveys such as the Health Survey for England or ELSA.Footnote 6

Direct comparison with the UK is inexact– for example, UK data refers to current or ex-smokers and the Danish study to daily smokers, but it is unclear how such differences affect the interpretation of the results. To find the total financial impact on society, all figures for individuals need to be scaled up to a population level and future costs need to take demographic and other changes into account.

The indications of this study are that economic benefits of smoking cessation are mainly generated in the wider economy – particularly differences in lifetime earnings, better health over the life course and tax receipts. This is important as it has previously been erroneously argued that tobacco duties offset lifetime health costs from smoking, but the Danish research shows otherwise.

Tobacco duties currently raise about £8.5 billion per year for the Treasury. Although receipts are down slightly on the two previous years, the total has been noticeably resilient to declining smoking prevalence rates and a tax escalator on tobacco prices. From a policy standpoint, the receipts are significant and would need to be replaced if, for example, tobacco were withdrawn from sale.

Smoking is already prohibited in most enclosed workplaces and public places in the UK. The Tobacco and Vapes bill going through parliament makes it an offence to sell tobacco products, herbal smoking products and cigarette papers to anyone born on or after 1 January 2009, hence gradually extending the ban over time.

How effective the policy will be is uncertain. Modelling work by the Department for Health and Social Care predicts that, without action, prevalence will level out at about 8% after 2035, but a lower rate would be needed to halve current prevalence by 2040. In addition, the predicted impact on the number of avoided deaths is low, which suggests the policy may need strengthening (Draper, Reference Draper2024).

3.2. Bringing It All Together

This section is based on the model commissioned by ASH from Landman Economics and summarises key findings based on costs and benefits (Reed, Reference Reed2024). Its value lies not only in the broader costs to society of smoking but also in individual components, including the impacts on public sector finances.

Table 2 shows the total UK loss due to lower productivity through lower employment and earnings plus associated impacts on gross value added, which is the value producers add to the goods and services they buy. These are called tangible costs and are measurable and can be computed from official statistics. These totalled £54.6 billion in 2023, of which England comprises £46.0 billion (row1+row2).

Table 2. The societal costs of smoking (£billions)

Table 2 includes a figure for intangible costs, which is an estimate of the costs of early deaths valued by QALYs. For men or women of each year of age, an average number of years of life lost is calculated using data from the ONS National Life Tables (Office for National Statistics, 2025). Intangible costs are not cashable in the same way as, for example, tobacco duties, but provide a measure of the social cost of earlier death.

These age- and sex-specific average number of years of life lost are converted into an average number of QALYs lost for men and women in each age year using tables in McNamara et al. (Reference McNamara, Schneider, Love-Koh, Doran and Gutacker2023), who calculate quality-adjusted life expectancy norms for the English population. The QALYs are then valued using the HMT Green Book (HMT, 2022) based on a suggested value of £70,000 per year.

In the evaluation this is then uprated to 2023 levels using the Consumer Price Index, giving a value per QALY of around £77,000 at 2023 prices. This gives an overall figure for the value of lives lost due to smoking-related illnesses of £38.3 billion for the UK as a whole and total societal costs of £93.0 billion per annum as shown at the foot of Table 2.

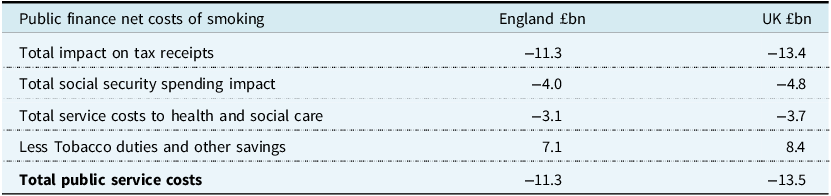

Table 3 shows the impact on public sector costs. The impacts are entered as negative amounts, indicating a worsening in public finances (i.e. net cost) compared with a non-smoking scenario. The first three rows show the effects on tax receipts, social security spending and the extra cost to health and social care.

Table 3. Net cost to public sector finances (£billions)

It shows that reduced tax receipts due to lower earnings for smokers worsened the UK Government’s fiscal position by just over £13.4 billion in 2023. Spending on in-work social security benefits is £4.8 billion higher than it would have been. It includes the extra costs of out-of-work, disability and income-related benefits, which include a small offset for reduced pension payments due to early death.

Finally, it shows £3.7 billion extra is spent on health and social care due to smoking-related causes, a small amount of which is for the cost to fire services attending smoking-related fires. This brings the total loss to £21.9 billion. The main offset to this figure is the £8.4 billion from receipts from tobacco duties increasing total net fiscal deficit to £13.5 billion.

3.3. Issues Arising

The tobacco case study shows the power of cost-benefit analysis. With potential tangible and intangible benefits of £93 billion, with potentially £54 billion worth of controllable costs, the financial case is clear. Of the total, £13.5 billion would be bankable savings to the exchequer, assuming the assumptions and calculations are broadly correct and the necessary policy changes are deliverable.

Because of time lags, delays in the necessary behavioural changes and economic adjustments, the policy will need to be finessed to avoid sudden drops in tobacco duties, slow uplift in tax receipts or falls in welfare and be sensitive to any growth of a black market in tobacco that would cause revenues to fall whilst not reducing smoking prevalence.

NHS and social care savings are notional. With a fixed NHS budget any efficiencies would be redeployed and be measured in terms of shorter waiting times or satisfying unmet need elsewhere in the health and care system. It is difficult to predict how this might play out without better efficiency metrics and cost attribution, as smoking affects so many aspects of people’s health.

The tobacco control policies recommended by the UK All-Party Parliamentary Group on Smoking and Health (APPG, 2023) are expected to reduce smoking prevalence by about one third during the next parliament, from about 11.4% in 2024 to 7.3% in 2029. It will be crucial to monitor progress once the Tobacco and Vapes Bill becomes law in case some provisions need strengthening and any adverse health impacts from vaping become clearer.

Extending the principles and learnings from tobacco control to other parts of the health economy is important, bearing in mind that it has taken decades to get to this point in the case of smoking. This is especially important given the ageing population, which will increase the overall burden of disease and therefore the demands on the health and care economy.

Table 4 is a simplified summary of health risks, the attendant dangers and types of intervention. Interventions tend to be generic but with some obvious differences. Chronic diseases are largely age and lifestyle related, with abstinence as the best intervention. Infectious diseases need close surveillance and rely on effective vaccines. Wider determinants of poor health lean toward non-medical interventions including regulation, health education and decent housing.

Table 4. A simple categorisation of health risks, dangers to people and the economy and intervention types

3.4. Accounting for Prevention

How much does the UK spend on prevention? Some areas of spending fall outside the remit of the NHS but are classified as prevention in the international system of health accounts. These can include spending by non-health government bodies such as the Food Standards Agency, Health and Safety Executive and Social Care and some private spending.

Of the £244 billion spend on health in 2022, £20.1 billion or 8.2% of the total was spent on prevention according to the ONS, down from 14.1% in 2021 during COVID. This is split roughly evenly between epidemiological surveillance, information and education, health monitoring, early disease detection and immunisation. The smallest category is on emergency response programmes to disasters.

It is contested whether all prevention spend is cost effective and that each category must be looked at on its own merits. Certainly, studies show that early cancer diagnosis, health checks and screening programmes can save lives; but cost attribution and the potential double counting of any savings can be an issue. In general, short-term cash releasing savings are valued more highly than long-term societal benefits.

Within this broad scope, prevention studies tend to be bespoke insofar as they are concerned with health outcomes, usually measured in years of life saved or QALYs. The causes of early deaths and consequent loss of life years are well-documented, but actions to reverse these are more hit and miss. Understanding risk factors whose avoidance would lower the age of onset of chronic diseases is clearly important.

Tobacco smoking shows the value of taking a life course approach since never smoking or stopping whilst young has considerably more health benefits than stopping later in life when much of the damage is done. Tobacco control acts as a potential template for large-scale prevention work where risk factors are identifiable and there is significant potential harm and public expenditure implications.

Other examples to which this applies could include obesity, mental health and substance abuse and are potential subjects for further investigations. Work in the US found that around 300,000 deaths per year are attributable to obesity, or about one tenth of all deaths (Allison et al, Reference Allison, Fontaine, Manson, Stevens and VanItallie1999). The same rate applied to UK data suggests attributable deaths of about 60,000 per year from obesity.

A study by Frontier Economics (2023) commissioned by the Tony Blair Institute for Global Change found that the societal costs of obesity were £98 billion a year, roughly the same as smoking. Of the total, £74 billion is due to obesity and £24 billion due to people being overweight. However, other estimates, such as those by the Health Foundation, are lower, which illustrates a lack of consistency.

Based on this approach, there are four stages to consider.

Stage one is understanding the scale and threat posed by a risk factor or risk factors, who they affect and the harm they cause. Risk exposure is controlled by the individual in the cases of smoking, obesity, alcohol consumption or lack of physical exercise. But exposure to wider determinants of ill health such as unemployment, homelessness and poor education are also important.

Stage two concerns how risks interact with the population at large, including their life cycle impact on health and life expectancy. Typically, we wish to evaluate the costs and benefits of an intervention, such as educating people on the dangers of alcohol. We need to understand how risks arise, over what period and the levels of harm caused, as well as the efficacy of any intervention.

Stage three involves evidence gathering on the costs of exposure and the financial impacts on individuals through changes in lifestyle, medication or other functional changes. The smoking case study included the direct costs to individuals such as lost earnings, care needs and, separately, the net impacts on public expenditure, such as lower tax receipts.

Stage four is the analytical phase – producing a balanced analysis of the costs and benefits of an intervention to reach a conclusion about its viability and effectiveness. While simple in principle, the substantive issues are mostly around data acquisition and quality, both of which are variable.

Data sources can include surveys, administrative systems, direct participant involvement or official data. National surveys are a good starting point for studies linking risk factors to broad health outcomes, provided they contain information on the risk factor or factors of interest, for example wider determinants like low income. Linked surveys can boost sample sizes and enable a longitudinal perspective (e.g. ELSAFootnote 7 ).

Using personal medical records is preferable in health evaluations, but the required data are dispersed among GP and hospital records and are difficult to access due to data protection reasons or to link together without a form of personal identifier. Anonymised clinical data sets are available but are weak on wider determinants such as lifestyle and other personal circumstances, and linkages to death registrations are incomplete.

Personal medical records can provide full medical histories and can be linked to other datasets such as hospital activity. In principle, it is possible to include costs of treatment using standard tariffs and prescription costs, although this is challenging. A good example of what can be achieved is provided by the Whole Systems Data Project, which linked hospital and GP records using NHS numbers (Mayhew & Harper, Reference Mayhew and Harper2019).

Whilst it would be nice to also link clinical data to social security payments, secure linkage, for example using National Insurance numbers, would be needed. However, the information stored about health in disability related benefits is limited and difficult to aggregate across health conditions, whilst access would require support from government statisticians in different departments and the NHS.

Actuaries can conduct studies that link health and financial parameters within insured populations. The same techniques could be applied to national studies if the data were in this form at a national level, as is already possible in Scandinavian countries. This offers a good way forward, but the challenge is unlocking commercially sensitive data to make it available for research purposes.

User participation sample-based data tends to be reserved for randomised control studies involving drugs or some other therapeutic intervention as used for example by NICE.Footnote 8 Samples are small, but in a well-constructed trial the findings can be generalisable to large populations. Recruitment and retention in these types of evaluations can be an issue.

The ONS produces large data sets at a national level that rely on surveys, the decennial census and official sources. Having separate statistical organisations in constituent countries of the UK can be a limiting factor, especially in small geographies. Economic and labour market coverage is good, but there is a lack of co-ordination with health and social care data, which is a major limitation.

4. Key Points and Next Steps

In summary, our paper has shown that policies that are effective in preventing harm and add to the collective societal good have great potential, but there is scope for improvement. Firstly, more examples of historical interventions are needed, looking at them through a wider “preventive lens” with a view to learning the lessons.

For example, mortality reductions in the early 20th Century were largely the result of housing improvements rather than the development of new treatments for diseases of poverty, which tended to come later (Charlton & Murphy, Reference Charlton and Murphy1997). A contemporary example might be building more homes for older people, thereby easing the shortage of homes for young families or improving health by adapting existing homes.

The silo nature of Government departments precludes data sharing and therefore the ability to challenge the supremacy of the medical model for improving health. We need more general-purpose data sets that combine ONS and NHS data at the individual person level, with the ability to aggregate up to the household and area levels – something we understand the ONS is pursuing.

Then, finally, there is the Scandinavian model. The UK does not keep registers like Scandinavian countries, which are kept continually up to date but with controlled access to their use. Data on this scale would provide scope for joined-up studies with multiple applications with faster turnaround and at lower cost. UK data sources such as Biobank are a step in this direction.

There is also a “make do” scenario in which we devise cleverer and more cost-effective ways of utilising the data resources we have – at least up to a point. This may be a topic for which actuarial skills may be appropriate – such as adding cost and time dimensions to prevention studies, but we are not aware of any examples of this.

From an actuarial perspective, the profession needs to be clearer on its research aims, whether it is providing a public good or if it is for its own benefit. Recent work on diabetes using personal medical records is a good example of insurers coming together with the aim of understanding the incidence and health trajectories of people diagnosed with diabetes, which could be shared publicly.

The profession also needs to learn from other disciplines, such as health economics, to understand how best to deploy its skills and make a difference. It is noteworthy, for example, that prevention, which crops up in cost-benefit analysis and risk, which is favoured by actuaries, are related mathematically. If one envisages an intervention aimed at saving lives or improving health, then we have this connecting identity:

$$\rm {Prevention \;gain = change \;in \;risk \times target \;population}$$

$$\rm {Prevention \;gain = change \;in \;risk \times target \;population}$$

What should it be focussing on? There are themes that regularly crop up in the public health literature (Faculty of Public Health, 2019), like addressing common risk factors, for example, smoking and obesity. Our preference would be to focus on studies where actuaries have a comparative advantage, all of which could help reduce pressures on the NHS and contribute to economic growth.

This could include strategies for reducing health inequalities, estimating the long-term health benefits of education, interventions that extend working lives or delaying the onset of long-term health conditions and multimorbidity. Linking the results to how they might improve NHS productivity would also be very valuable.

One approach is to set up a monetary baseline of prevention activities using a common taxonomy (The Health Foundation, 2024; O’Brien & Charlesworth, Reference O’Brien and Charlesworth2024). This could be linked to a dashboard of metrics such as health expectancy, inequalities, smoking, obesity, avoidable deaths and others, alongside economic metrics. A good example of this is HAPI, the global Healthy Ageing and Prevention Index produced by ILC-UK.Footnote 9

Is prevention a lifeline to the NHS or not, as suggested in the title? This paper affirms that it is. However, it finds that the value of prevention is dispersed across a wide range of activities, government departments and agencies and is not centrally compiled or coherent. It is also abundantly clear that the challenge to improve that health and well-being of the population is not something that the NHS can achieve on its own.

Health improvements accrue very slowly, as seen in the case of tobacco. Some of the biggest challenges, like levelling up inequalities, are outside the control of the NHS and require behavioural change, legislation and investment. Political and business interests are not always aligned with the public good because of differences in the political and business cycles, which are shorter-term.

There are definitional and methodological challenges to consider for prevention to take root in a policy context. Some of the more important interventions, such as the supply of good quality housing, have yet to feature in the debate and so a holistic approach including a better monitoring framework is needed. With co-ordinated effort, these problems could be overcome.

The actuarial profession can join this debate in three ways: first, using its analytical skills to improve how the financial returns on prevention policies can be best quantified; second, finding ways of using industry data for the general good, for example highlighting the impact of wider determinants on health and mortality; third, by funding a research programme leading to an actuarial qualification in prevention or including prevention in the actuarial curriculum.

Disclaimer

The views expressed in this publication are those of invited contributors and not necessarily those of the Institute and Faculty of Actuaries. The Institute and Faculty of Actuaries do not endorse any of the views stated, nor any claims or representations made in this publication and accept no responsibility or liability to any person for loss or damage suffered as a consequence of their placing reliance upon any view, claim or representation made in this publication. The information and expressions of opinion contained in this publication are not intended to be a comprehensive study, nor to provide actuarial advice or advice of any nature and should not be treated as a substitute for specific advice concerning individual situations. On no account may any part of this publication be reproduced without the written permission of the Institute and Faculty of Actuaries.

Open access

Open access